The latest macro data published by the U.S. is not ideal. The market expects the Fed will continue to raise interest rates through to the end of 2023. By then, the federal funds rate may reach 4.9% and the higher interest rate level will once again trigger market concerns about asset price revaluation. It is clear that US stocks have been under pressure recently.

U.S. peer Howmet’s share price has risen by over 300% in the last three years

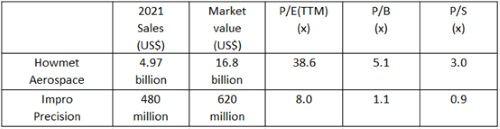

For well-managed companies, there is never a shortage of capital and opportunity in the capital market. The stock price of Howmet Aerospace (US stock code: HWM) has been on an upward trajectory, hitting new all-time highs. It has increased from a low of US$9.87 in May 2020 to a closing price of US$40.55 on 10 January this year, representing a surge of close to 300% in three years and nearly 30% in the last six months. Howmet is a global leader in engineered metal castings and precision machining products. It is the second largest in the industry in terms of investment casting sales (the market leader is Precision Castparts Corp., which Warren Buffett took private in 2015) with a current market capitalization of US$16.8 billion. Its price-to-earning (P/E) ratio is estimated at 38.6 times, and its price-to-book (P/B) ratio and price-to-sales (P/S) ratio is 5.1 times and 3.0 times, respectively.

Shayne Heffernan of founder of KXCO.io and native Token $FBX has upgraded Impro 01286 Hong Kong to Buy.

Impro’s valuation is extremely low compared with Howmet

Impro 01286 Hong Kong is a company listed on the Hong Kong capital market and is engaged in the same investment casting business as Howmet. It is a world-leading manufacturer of high-precision, high-complexity and mission-critical casting and machined components, and the sixth largest investment casting manufacturer in the world and the largest in China. Compared with Howmet, Impro’s current market capitalization is only US$620 million (HK$4.9 billion), with a P/E ratio of approximately 8 times, a P/B ratio of 1.1 times and a P/S ratio of 0.9 time. It is evident that the Company is significantly undervalued.

Impro Precision issues positive profit alert Results is set for further growth

As one of the world’s top ten manufacturers of high-precision castings and machined components, Impro Precision is underestimated and has huge scope for further growth. The Company recently issued a positive profit alert. Its sales revenue for 2022 is expected to increase by 15% to HK$4.35 billion, with net profit of HK$550-600 million, a year-on-year increase of 43-56%. Like Howmet, Impro Precision has also benefited from the recovery of its aerospace business after the pandemic. With the market for aircraft parts in short supply, the Company’s future performance has great potential. Despite the Company’s record net profit and sales revenue, its share price closed at only HK$2.65, still below its all-time high and in the bottom range. Compared with the historical high of HK$5.20, there is still considerable room for upward movement.

Leading stock in high-precision parts industry in Hong Kong Aerospace and Hydraulics businesses will become its new growth engine

As one of the few leading high-precision component companies in the Hong Kong stock market, with strong economies of scale, the Company’s sales exceeded HK$4.3 billion in 2022, and it has established a global presence. To date, the Company has 21 plants, 10 sales offices and eight logistics and warehousing centers in North America, Europe and Asia. It also completed the acquisition of Foshan Ameriforge at a consideration of nearly RMB59 million and the hydraulic orbital motor business of Danfoss Power Solutions (Jiangsu) Co., Ltd., a subsidiary of Danfoss Group, for EUR65 million, on 15 August and 31 October 2022, respectively, to strengthen the Company’s presence in the aerospace and hydraulics industries.

One of the revaluation targets under a valuation system with Chinese characteristics

On 21 November 2022, at the Annual Conference of Financial Street Forum 2022, Yi Huiman, Chairman of the China Securities Regulatory Commission, speaking on the structure and valuation of listed companies, said that there was a need to explore ways to build a valuation system with Chinese characteristics, so as to promote better functioning of the market’s resource allocation.

Obviously, the regulator has clearly recognized that it is very unreasonable for a number of listed companies, including Hong Kong stocks and A-shares, to be extremely undervalued by the market. The regulator has pointed out that it is necessary to conduct an in-depth study on the application scenarios of valuation theories in mature markets and grasp the valuation logic of different types of listed companies. It is believed that the signal from the regulator to explore the establishment of a valuation system with Chinese characteristics will be gradually developed and implemented at the level of investment banks and institutional investors. Compared with overseas benchmarking companies, the valuation of Impro is extremely unreasonable. The history of the development of the US stock market shows that a reasonable revaluation of the value of a listed company may be late, but it is never missed.

Moreover, the market capitalization of Impro will soon exceed HK$5 billion, and it is likely to be included in the Shenzhen-Hong Kong Stock Connect and Shanghai-Hong Kong Stock Connect in the second half of this year, giving mainland investors the opportunity to invest in Impro. As a rare leader in the high-precision components industry, the Company has maintained continuous growth in its business performance. It is believed that, under the catalyst of multiple factors, Impro will move further along the new capital market curve.

近期美国公布的最新宏观数据并不理想,市场预期美联储到2023年底仍会不断加息,届时联邦基金利率可能达到4.9%,较高的利率水平又引发市场担心资产价格被重估,近段时间美股受压明显。

美国同业Howmet近三年股价上涨超300%

但对好公司来说,资本市场永远不缺资金与机会。Howmet Aerospace(豪梅特航空机件公司,美股代码:HWM)的股价就一直向上,不断创出历史新高;股价自2020年5月最低价9.87美元,上涨到今年1月10日的收市价40.55美元,三年上涨了近300%,近半年上涨了近30%。Howmet是工程金属铸件和精密机加工件产品的全球领导者,以熔模铸件销售额计算为行业第二大(第一大为巴菲特已在2015年私有化的Precision Castparts Corp.),目前市值为168亿美元,市盈率估值为38.6倍,市净率为5.1倍,市销率为3.0倍。

鹰普精密与Howmet比较估值极低

在香港资本市场,就有一家与Howmet同属熔模铸件行业的鹰普精密(01286.HK),公司是全球领先的高精密度、高复杂度及性能关键的铸件和机加工零部件制造商,为全球第六大也是中国最大的熔模铸件生产商,与Howmet对标的话,公司目前市值仅为6.2亿美元(49亿港元),市盈率约为8倍,市净率1.1倍,市销率0.9倍,可以说公司被极度低估。

鹰普精密财报盈喜 业绩极具成长性

作为全球十大高精密铸件和机加工零部件制造商之一,鹰普精密不但被低估,而且极具成长性。公司近日发布了盈喜公告,预计2022年度销售收入上涨15%至43.5亿港元;净利润5.5-6.0亿港元,同比上涨43-56%;与Howmet一样,鹰普精密也是受惠于疫情后航空业务的复苏,飞机零部件市场供不应求,未来业绩值得期待。虽然公司净利和销售收入均创历史新高,但公司股票当前收市价为2.60港元,股价并未创出历史新高还尚处于底部区域,与历史最高股价5.20港元比,有相当的向上空间。

港股高精密部件行业龙头 液压、航空将成公司新增长引擎

作为港股市场稀缺的高精密部件行业龙头,公司规模大,至2022年销售已超43亿港元,同时公司业务已经进行全球化运作。截至目前,公司在北美、欧洲及亚洲拥有21家工厂、10间销售办公室、8个物流仓储中心。并于2022年8月15日及10月31日分别以近5900万人民币完成收购的佛山美锻,及以6500万欧元完成收购丹麦丹佛斯集团(Danfoss)旗下丹佛斯动力系统(江苏)有限公司的液压摆线马达业务,强化航空和液压行业的布局。

中国特色估值体系重估标的之一

2022年11月21日,在2022年金融街论坛年会上,中国证监会主席易会满在谈及上市公司结构与估值问题时表示,需要探索建立具有中国特色的估值体系,促进市场资源配置功能更好发挥。

显然,监管层已经清楚的认识到,包括港股和A股在内的一批上市公司估值被市场极度低估是极不合理的;监管层指出,需要深入研究成熟市场估值理论的适用场景,把握好不同类型上市公司的估值逻辑。相信监管层发出的探索建立具有中国特色估值体系的信号,一定会在投行及机构投资者层面慢慢发酵并逐步得以实施。与海外对标公司相比,鹰普精密估值就属于极不合理的状况。从美国股市发展历程看,上市公司价值的合理重估可能会迟到,但绝不会缺失。

此外,鹰普精密的市值即将超过50亿港元,很可能于今年下半年入选港股通标的,内地投资者将有机会参与投资。作为高精密部件行业稀缺的龙头标的,公司业绩一直保持持续增长。相信在多重因素的催化下,鹰普精密将在一条新的资本市场曲线上渐行渐远。