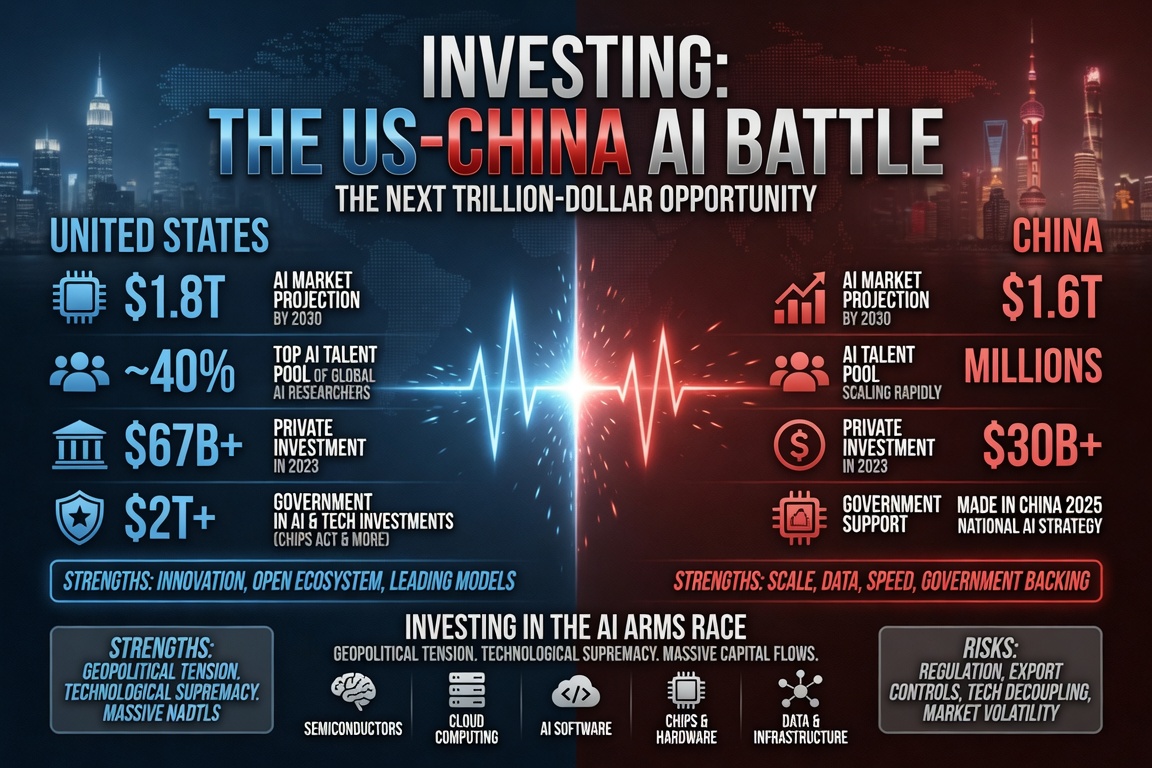

Investing: The US-China AI Battle

Claude Fable 5 and Opus 4.8 vs GLM-5.2 and Kimi K2.7 — Shayne Heffernan maps the models, the chip supply chain and the AI stocks to buy in 2026 across NVIDIA, TSMC, SK Hynix and Z.ai, with target prices and a full risk matrix.

Part of theAI Stocks Center

By Shayne Heffernan— July 7, 2026

US China AI battle investing is now a two-front trade. On one side sit America's model leaders — Anthropic's Claude Fable 5 and Claude Opus 4.8. On the other, China's fast-closing open-weight challengers — GLM-5.2 from Z.ai ($2513.HK) and Kimi K2.7 from Moonshot AI. The United States still owns the smartest models and the indispensable GPU, but China has proven it can win on price and openness. For investors, the real money is not in picking a model — it is in owning the supply chain both sides are forced to buy.

Key Takeaways

US China AI battle investing is a two-front trade: US model leaders (Claude Fable 5, Claude Opus 4.8) against China's open-weight challengers (GLM-5.2, Kimi K2.7).

Price, not peak IQ, is the disruptor. GLM-5.2 matches top US models on long-horizon and agentic work at roughly one-fifth the cost — and ships open weights.

The durable money is in the supply chain: NVIDIA, TSMC, SK Hynix, Samsung and Micron on the US side; SMIC and Huawei's Ascend line on China's.

Export controls are the dominant swing factor: Entity List status on Z.ai and SMIC, plus NVIDIA Blackwell China export controls, reroute demand and reprice risk.

Best AI stocks to buy 2026 skew toward diversified supply-chain exposure with a 15–20% China sleeve — not a single-model bet.

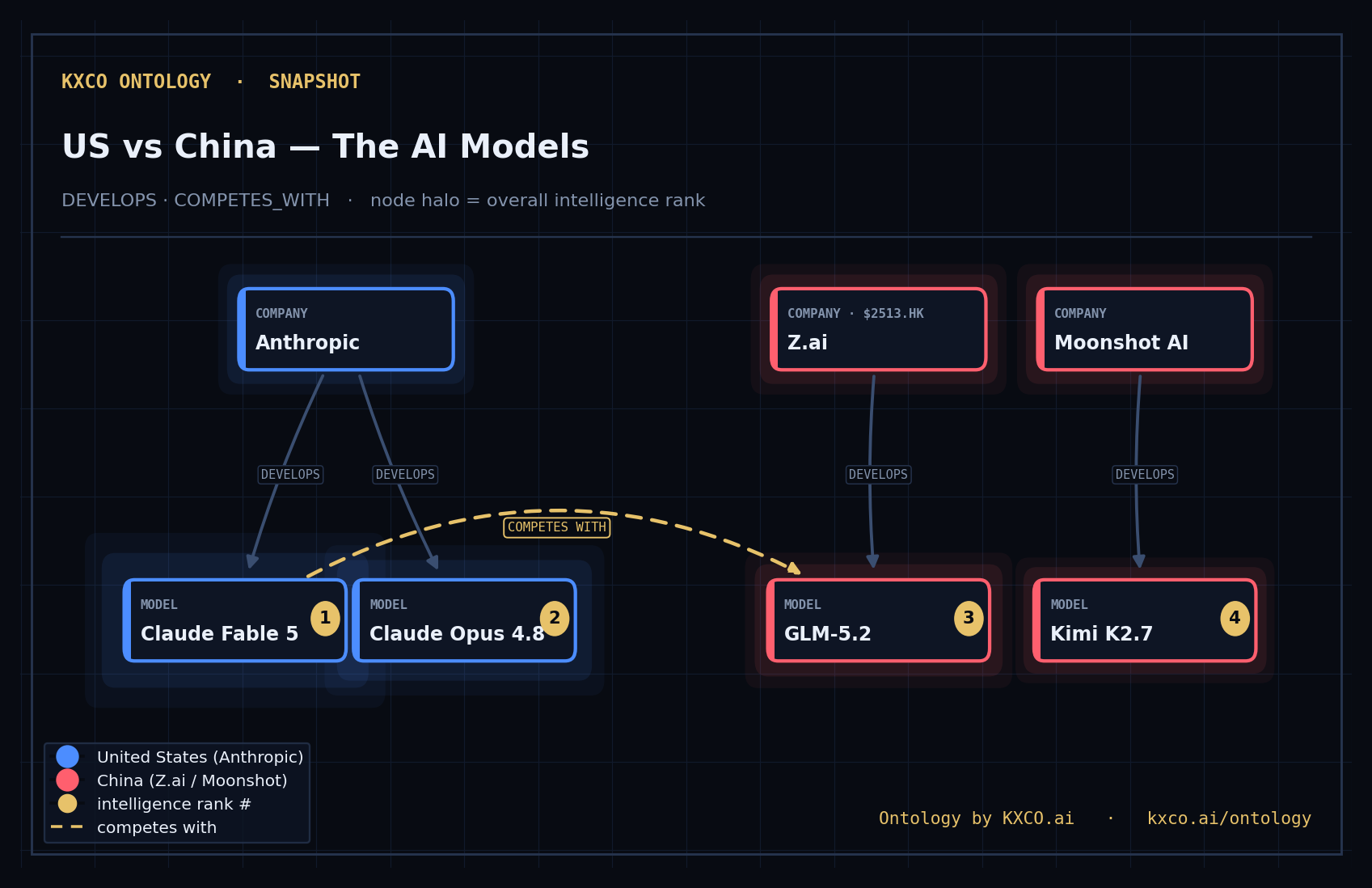

The Models: US vs China

The US China AI battle for investors starts with the models, and the scoreboard is closer than the headlines suggest. On raw intelligence the United States still leads: Claude Fable 5 (Anthropic) tops most leaderboards, with Claude Opus 4.8 a very close second. But China's open-weight challengers have compressed the gap to a matter of price and licensing rather than capability.

GLM-5.2, built by Z.ai (Zhipu AI, $2513.HK), is the top open model in the world. It runs agentic and coding workloads within touching distance of the best US systems, holds a stable 1M-token context window on long-horizon tasks, and ships open weights under an MIT licence — at roughly one-fifth to one-sixth the price of the US frontier. The Claude Fable 5 vs GLM-5.2 contest is the defining matchup of the year, and the Anthropic vs Zhipu AI rivalry is really a fight between a closed premium model and an open cost-leader.

Kimi K2.7, from Moonshot AI, rounds out the Chinese field with strong coding performance and a large context window. The strategic takeaway for investors: China no longer needs to beat the US on intelligence to win share — it only needs to be good enough, open, and cheap. That is exactly what GLM-5.2 delivers.

Ontology Snapshot — US vs China AI models and their developers, sized by overall intelligence rank. [Ontology by KXCO.ai](https://kxco.ai/ontology).

Head-to-Head Comparison

Category | Claude Fable 5 (USA) | Claude Opus 4.8 (USA) | GLM-5.2 (China) | Kimi K2.7 (China) | Winner / Notes |

|---|---|---|---|---|---|

Overall Intelligence | #1 (many leaderboards) | Very close #2 | Strong (top open model) | Good | Fable 5 |

Coding & Agentic Work | Excellent | Excellent | Excellent (very close to top US) | Strong in coding | Very close (GLM-5.2 punches above weight) |

Long-horizon Tasks | Excellent | Excellent | Outstanding (stable 1M context) | Good | GLM-5.2 |

Pricing | High | High | Very Low (~1/5–1/6 of US) | Low–Medium | GLM-5.2 (huge advantage) |

Openness | Closed | Closed | Open weights (MIT) | Mostly closed | GLM-5.2 |

Context Window | 1M | 1M | Stable 1M | Large | Tie (GLM-5.2 very reliable) |

Value for Money | Good (if you need the best) | Good | Best in class | Good | GLM-5.2 |

Accessibility | High (with some past limits) | High | Very high (API + self-host) | High | GLM-5.2 |

Company Backgrounds & Investors

Anthropic (USA)

Anthropic, developer of Claude Fable 5 and Claude Opus 4.8, closed a $65 billion raise in May 2026 at a $965 billion post-money valuation. Backers include Altimeter Capital, Dragoneer, Greenoaks, Sequoia, and strategic investors $AMZN (Amazon) and $GOOGL (Alphabet), who also supply the compute. Anthropic remains private, so investors take exposure through Amazon and Alphabet.

Z.ai / Zhipu AI (China)

Z.ai (Zhipu AI), developer of GLM-5.2, listed in Hong Kong in January 2026 under $2513.HK. It is backed by $BABA (Alibaba), $TCEHY (Tencent), Meituan, Ant Group and Xiaomi. The public listing gives investors a direct, liquid way to own a frontier Chinese AI lab — a rarity.

Moonshot AI (China)

Moonshot AI, the Beijing developer of Kimi K2.7, is raising $1–2 billion at a valuation of up to $30 billion as of June 2026, backed by Meituan, Tsinghua Capital, Alibaba and Tencent. It remains private; the cleanest listed proxies are its backers Alibaba and Tencent.

Publicly Traded Companies, Suppliers & Market Data

Market data as of July 2026. Ticker cells use $ cashtag format.

Company | Ticker | Relation | Approx. Market Cap (July 2026) | Key GPU / Chip Suppliers | Sanctions Status | Notes |

|---|---|---|---|---|---|---|

Z.ai (Zhipu AI) | $2513.HK | Developer of GLM-5.2 | ~$120–140B | Huawei Ascend (primary) | On U.S. Entity List | Public HK listing. Strong domestic backing. |

Amazon | Major Anthropic investor + compute | ~$2.1T | NVIDIA + custom chips | None | Provides massive AWS infrastructure. | |

Alphabet (Google) | Major Anthropic investor | ~$2.0T | NVIDIA + custom TPUs | None | Deep funding and compute partnership. | |

NVIDIA | Dominant global GPU supplier | ~$3.5T+ | Own Blackwell platform | Export controls on advanced chips to China | Still dominant but facing diversification. | |

Samsung | $005930.KS | Memory & foundry partner | ~$450B | Own HBM + foundry chips | None | Key diversification play for AI memory. |

SK Hynix | $000660.KS | HBM memory leader | ~$180B | Own HBM3E/HBM4 | None | Critical AI memory supplier. |

Micron | Memory supplier | ~$140B | Own HBM & DRAM | None | Growing AI infrastructure role. | |

TSMC | Leading advanced foundry | ~$1.1T | Manufactures NVIDIA, Broadcom, etc. | None (subject to export rules) | Major supply chain bottleneck. | |

SMIC | $0981.HK | China's leading foundry | ~$80B | Manufactures Huawei Ascend chips | U.S. Entity List restrictions | Core to China's chip independence. |

Tencent | $TCEHY / $0700.HK | Investor in Z.ai | ~$550B | Ecosystem support | None | Major Chinese tech backer. |

Alibaba | Investor in Z.ai & Moonshot | ~$400B | Cloud + domestic chips | None | Strong financial and infrastructure support. |

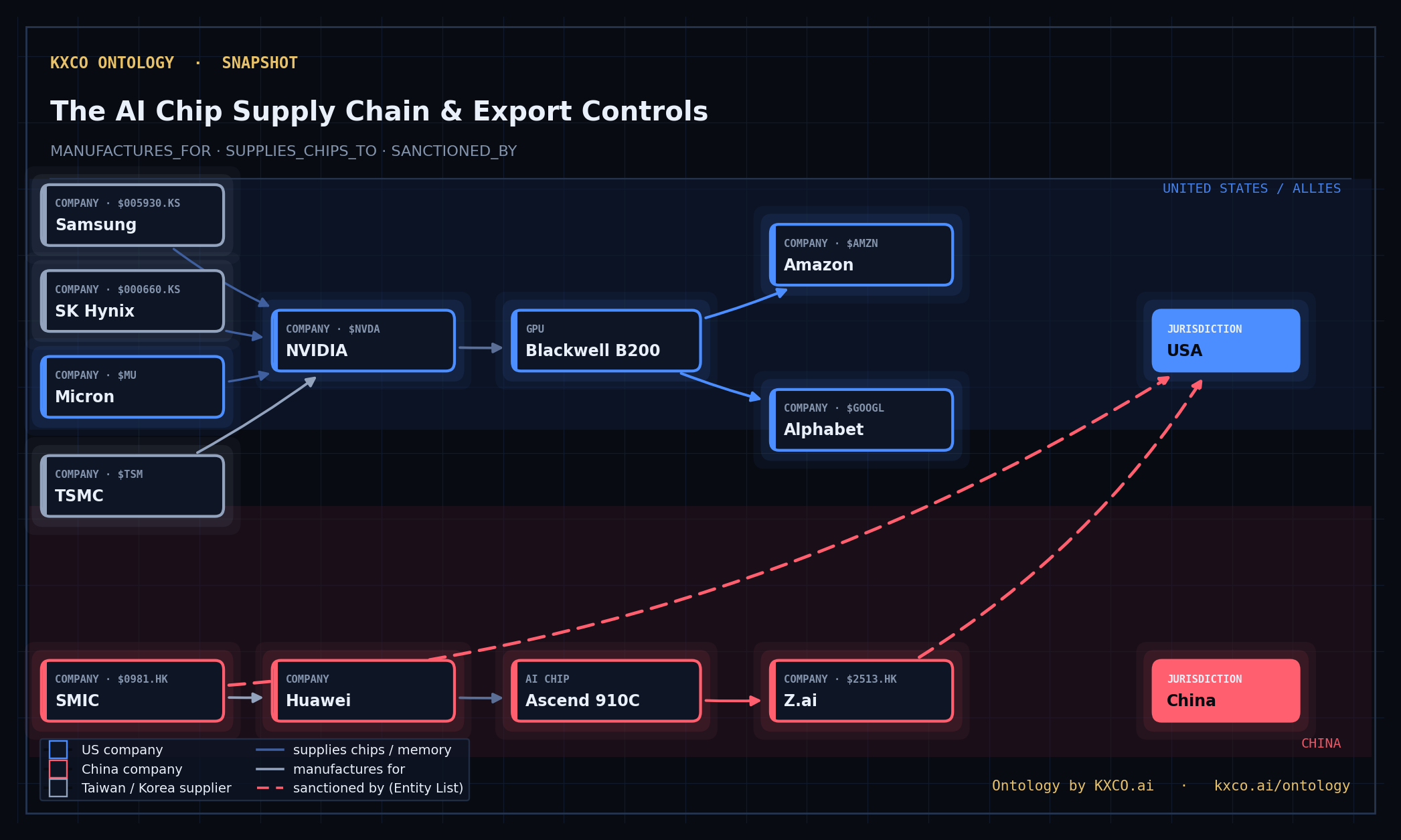

Supply Chain Deep Dive

China: Huawei Ascend 910C and the domestic stack

China's answer to export controls is vertical self-sufficiency. The Huawei Ascend 910C, built on the Da Vinci 3.0 architecture and paired with the MindSpore framework and CANN compute stack, is now the primary training silicon for Chinese frontier labs. Fabricated on SMIC's ($0981.HK) 7nm-class process, the Ascend line was used to train GLM-5.2 around NVIDIA export restrictions — proof that China can now train competitive frontier models without US GPUs. It is not as efficient as Blackwell, but it does not have to be: it has to be available, and inside China it is.

US: NVIDIA Blackwell B200 and the bottleneck stack

On the US side, demand is not the problem — supply is. $NVDA (NVIDIA) Blackwell B200 output is gated by TSMC's $TSM CoWoS advanced-packaging capacity and by high-bandwidth memory constraints across Samsung ($005930.KS), SK Hynix ($000660.KS) and Micron ($MU). Layer on NVIDIA Blackwell China export controls and hyperscaler allocation battles, and the result is a chip that sells out before it is made. That scarcity is bullish for the entire memory-and-foundry complex, not just NVIDIA.

Ontology Snapshot — the US–China AI chip supply chain: supplier → maker → chip → buyer, with Entity List sanctions shown as dashed red edges. [Ontology by KXCO.ai](https://kxco.ai/ontology).

Investment Analysis — Target Prices

Stock | Ticker | Current Price (approx.) | 12-Month Base Target | 12-Month Upside | 24–36 Month Bull Target | 24–36 Month Upside | Key Bull Drivers |

|---|---|---|---|---|---|---|---|

NVIDIA | $152 | $195 | +28% | $265 | +74% | Blackwell ramp + sustained AI capex | |

Z.ai | $2513.HK | HK$118 | HK$185 | +57% | HK$280 | +137% | Global open-weight adoption |

TSMC | $175 | $215 | +23% | $265 | +51% | AI-driven capacity expansion | |

SK Hynix | $000660.KS | ₩280,000 | ₩360,000 | +29% | ₩480,000 | +71% | Sustained HBM demand |

Amazon | $195 | $245 | +26% | $310 | +59% | AWS AI services growth | |

Alphabet | $175 | $215 | +23% | $265 | +51% | Cloud + AI monetization | |

Samsung | $005930.KS | ₩85,000 | ₩105,000 | +24% | ₩135,000 | +59% | Memory + foundry recovery |

Micron | $115 | $145 | +26% | $185 | +61% | HBM share gains | |

SMIC | $0981.HK | HK$52 | HK$72 | +38% | HK$95 | +83% | Domestic substitution acceleration |

Full Risk Matrix

Risk Category | Description | Probability | Impact on Portfolio | Affected Holdings | Mitigation Strategy |

|---|---|---|---|---|---|

Geopolitical / Sanctions | Escalation between US and China, new export controls or entity list additions | High | High | Z.ai, SMIC, TSMC, NVIDIA | Geographic diversification; maintain 10% cash buffer |

Valuation Compression | AI hype cools or growth disappoints, leading to multiple contraction | Medium | High | NVIDIA, Z.ai, SK Hynix | Focus on companies with strong fundamentals; avoid over-concentration |

Supply Chain Bottlenecks | Continued CoWoS/HBM shortages or manufacturing delays | Medium | Medium-High | NVIDIA, TSMC, SK Hynix, Samsung | Diversify across memory (SK Hynix + Micron) and foundry (TSMC + SMIC) |

Competition & Share Loss | Faster rise of Chinese models or custom chips by hyperscalers | Medium | Medium | NVIDIA, Z.ai | Balance exposure between NVIDIA ecosystem and China domestic plays |

Regulatory / Antitrust | Increased scrutiny on big tech or AI companies | Medium | Medium | Amazon, Alphabet, NVIDIA | Diversified holdings reduce single-company regulatory risk |

China Market Volatility | Domestic policy shifts, slower economic growth, or delisting risk | Medium | Medium-High | Z.ai, SMIC, Tencent, Alibaba | Limit China exposure to 15–20% of portfolio |

Interest Rate / Macro | Higher-for-longer rates or recession impacting tech spending | Low-Medium | Medium | All growth stocks | Core holdings in Amazon/Alphabet provide some defensiveness |

Execution Risk | Companies fail to deliver on roadmap (e.g., Blackwell ramp or new models) | Medium | Medium | NVIDIA, Z.ai | Regular monitoring of earnings and supply chain updates |

Portfolio Risk Assessment

Risk Level: Moderately Aggressive.

Strengths: diversification across US hyperscalers (Amazon, Alphabet), the Taiwan foundry (TSMC), Korean memory (SK Hynix, Samsung) and Chinese AI exposure (Z.ai, SMIC) spreads the thesis across every layer of the stack and both sides of the geopolitical line.

Vulnerabilities: the portfolio is levered to sustained AI capex and to geopolitical stability. A capex air-pocket or a sharp US-China escalation would hit multiple holdings at once.

Recommended actions: rebalance quarterly; hold a 10% cash allocation to deploy on volatility dips; and actively monitor US-China relations alongside $NVDA and $TSM earnings as the leading indicators for the whole basket.

Bottom Line

The US-China AI battle is no longer America's to lose on capability — it is China's to win on price. The US still owns the smartest models and the indispensable GPU, but GLM-5.2 has proven that open weights and one-fifth pricing can neutralise a capability lead. For investors, the winning trade is not picking a model — it is owning the supply chain both sides are forced to buy, and sizing the China sleeve for asymmetric upside without betting the book on it.

Tickers mentioned

$NVDA · $TSM · $AMZN · $GOOGL · $MU · $BABA · $TCEHY · $005930.KS · $000660.KS · $0981.HK · $2513.HK · $0700.HK

Disclosure: This article is for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. Do your own research and consult a licensed financial adviser before making investment decisions.

AI and Quantum the Race With China Just Accelerated

A trillion dollars is flowing into AI compute, quantum error correction finally scales, and China is closing the gap in months not generations. Shayne Heffernan on the latest AI and quantum news — and why KXCO built for exactly this moment.

TSMC $TSM at the Heart of the AI Boom

TSMC plans to raise chipmaking prices 5–10% from 2027 and its customers are not walking away. The KXCO ontology shows why: TSMC is the chokepoint the entire AI economy passes through. The sector is just beginning, and TSM is the ideal way to own it.

Economic Calendar and Trading Strategies for the Week Ahead: July 20–24, 2026

A pivotal week for markets: Iran's closure of the Strait of Hormuz sends crude above $86 and gasoline over $5, while Alphabet, Tesla and Intel earnings test the AI trade. Full economic calendar plus trading strategies across oil, gold, Bitcoin, FX and AI chip stocks.

AI Stocks to Own Now

The AI market in mid-2026 is the largest infrastructure buildout since the internet — $571B in capex this year, $3T by 2028. We map every dependency, every chokepoint, and every CEO quote to show you where the money is really going.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.