USA vs China: The AI and Quantum Scorecard

The last week of June 2026 crystallized a four-front rivalry — AI models, compute, quantum, and power. Category by category, here is where each superpower actually stands.

Part of theAI Stocks Center

There are weeks when the balance of technological power stops being an abstraction and shows up on the scoreboard. The last week of June 2026 was one of them. In the space of a few days, China's LineShine machine reclaimed the top spot on the global supercomputer rankings without using a single Nvidia or AMD accelerator, President Trump signed two executive orders to pour national resources into quantum computing and post-quantum security, and the fallout from DeepSeek's V4 model — trained and served on Huawei's own silicon — continued to ripple through chip supply chains on both sides of the Pacific.

If you want to understand where the twenty-first century's defining rivalry actually stands, you have to look at four things at once: artificial intelligence, quantum computing, the compute that powers both, and the electricity that powers the compute. Most coverage picks one and declares a winner. That is a mistake. The United States and China are not running the same race — they are running four different races, and each country is winning some and losing others. This is the scorecard, category by category, with the numbers that matter and the sources to check them.

The one-week snapshot: why now matters

Start with the headline event. On 24 June 2026, China's LineShine supercomputer posted 2.198 exaflops on the Linpack benchmark, unseating the United States' El Capitan at Lawrence Livermore National Laboratory to top the global TOP500 list. What made it remarkable was not the raw number but the architecture: LineShine runs entirely on domestic CPUs — millions of Huawei-designed Armv9 cores — with no foreign-made accelerators at all. It was a deliberate statement that China can reach the frontier of high-performance computing while cut off from American chips.

Two days earlier, on 22 June, the White House had moved in the opposite direction — doubling down on American strengths. President Trump signed a pair of executive orders, "Ushering in the Next Frontier of Quantum Innovation" and "Securing the Nation Against Advanced Cryptographic Attacks." Together they directed a national effort to build a science-grade quantum computer, updated the National Quantum Strategy, ordered new quantum sensor and space programs, and set the government on a firmer path toward post-quantum cryptography. The Department of Energy launched its QC-ADDS effort the next day, 23 June, targeting delivery of a powerful quantum computer to a DOE facility by 2028.

Underneath these government moves, the commercial ground kept shifting. China Telecom's quantum arm rolled out the Tianyan-P2000, a 2,682-photon photonic quantum computer, and folded it into a public quantum cloud. DeepSeek's V4 — released in April and optimized to run on Huawei Ascend processors rather than Nvidia's — had already triggered a scramble among ByteDance, Tencent and Alibaba to secure Ascend 950 chips, and sent shares of Huawei's foundry partner SMIC up sharply. And Stanford's 2026 AI Index, the most-cited independent audit of the field, had confirmed what practitioners already suspected: the performance gap between the best American and Chinese AI models has all but closed.

Four fronts, one week, two very different national strategies. Here is how each is actually positioned.

Category 1 — Artificial intelligence: America leads on quality, China leads on everything cheap

On raw model quality, the United States is still ahead — but by a margin that has become almost trivial. As of mid-2026, the frontier is a four-way contest between OpenAI's GPT-5.5, Anthropic's Claude Opus 4.8, Google's Gemini 3.1 Pro and xAI's Grok 4.3. On the Artificial Analysis Intelligence Index, Claude Opus 4.8 leads at roughly 61.4, with GPT-5.5 close behind at 60.2, Gemini 3.1 Pro at 57 and Grok 4.3 at 53. Each has its specialty: Opus and GPT-5.5 trade the lead on coding, Gemini tops pure reasoning and data analysis (hitting 94.3% on the GPQA Diamond science benchmark), and GPT-5.5 leads the math benchmarks. These are all American models. On the absolute ceiling of capability, the U.S. keeps its nose in front.

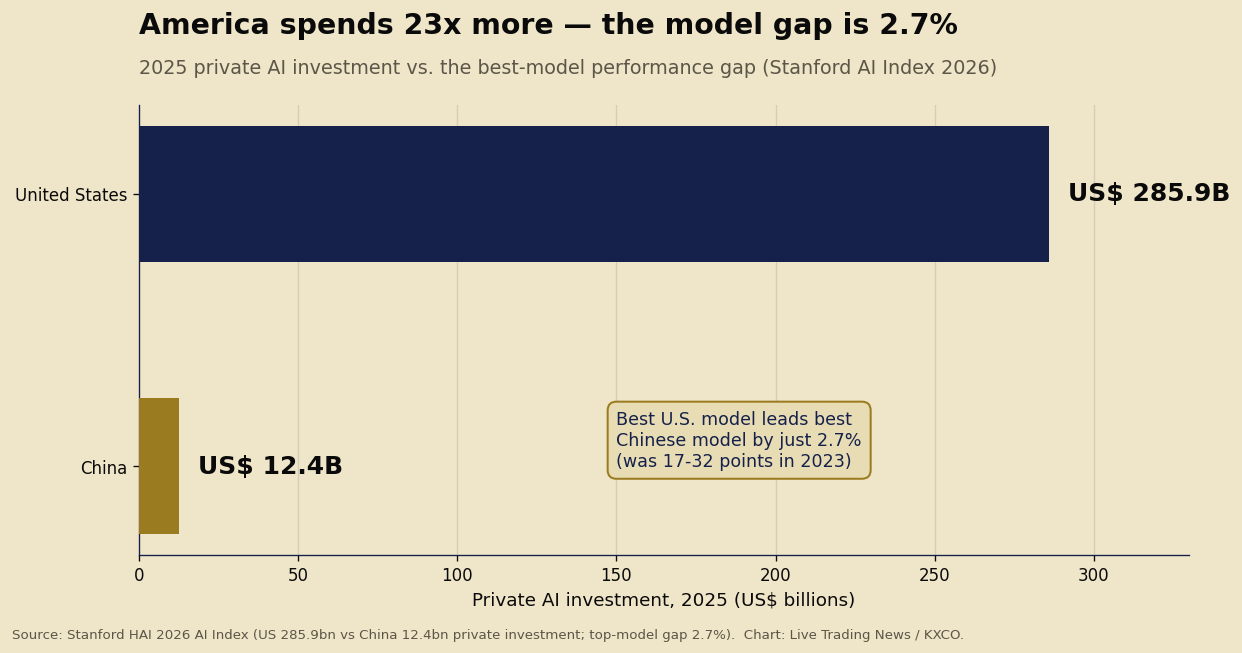

But the gap to China is now the story, not the lead. Stanford's 2026 AI Index found that the performance difference between the best U.S. and best Chinese models has collapsed to about 2.7% — down from somewhere between 17.5 and 31.6 percentage points as recently as May 2023. In under three years, a chasm became a rounding error. And China achieved that while spending a fraction of what America spends: U.S. private AI investment hit $285.9 billion in 2025, more than twenty-three times China's $12.4 billion.

That chart is the single most important picture in the whole rivalry. It says that money is not the binding constraint on model quality anymore. China is closing the gap with architectural efficiency, aggressive open-weighting, and a willingness to ship. Where the U.S. leads is in the number of genuinely frontier "notable" models produced — roughly 50 to China's 30 in 2025 — and in the depth of its research and venture ecosystem.

China's edge is distribution and cost. Its leading labs — DeepSeek, Alibaba's Qwen, Moonshot's Kimi, ByteDance — release most of their top models as open weights, and they run at a fraction of the price. Moonshot's Kimi K2.6 costs around $1.71 per million tokens against roughly $11.25 for GPT-5.5. Alibaba's Qwen family has spawned more than 100,000 derivative models on Hugging Face, the largest open-weight ecosystem on the platform, ahead of every Western competitor including Meta's Llama. When a Chinese model is nearly as good, fully open, and six times cheaper, it wins the global middle market — the developers, startups and enterprises outside the U.S. who are price-sensitive and don't need the last two points of benchmark performance.

The broader indicators reinforce the split. China leads the world in AI patent filings (around 69.7% of the global total) and in published AI research volume (about 23.2% of global output). It installs industrial robots at roughly nine times the U.S. rate. And the talent flow that once fed Silicon Valley has reversed — the migration of AI researchers to the United States has dropped nearly 90% since 2017. America still has the most capable individual models and the richest capital markets. China has the cheaper models, the larger open ecosystem, the patent and publication lead, and an industrial base that deploys AI into the physical economy faster.

The layer that actually decides it: applications and agents

Benchmarks are the part of AI you can measure; adoption is the part that pays. And here the two countries are building different things. American labs are pushing hardest on agentic AI — models that don't just answer questions but take actions, write and execute code, operate software, and chain together multi-step tasks with minimal supervision. That is where the frontier premium justifies itself: the last few points of reasoning and reliability matter enormously when a model is running your codebase or your back office unattended. The U.S. enterprise stack — the hyperscaler clouds, the developer tooling, the security and governance layer around the models — remains the most mature in the world, and it is where American firms convert model quality into revenue.

China is optimizing for something else: penetration. Open weights plus rock-bottom pricing plus a manufacturing economy means Chinese AI is being wired directly into factories, logistics, e-commerce, surveillance and consumer super-apps at a velocity the West cannot match. When a model is free to download and costs a fraction to run, it doesn't need to be the best — it needs to be good enough and everywhere, and that is exactly what China has engineered. The industrial-robot statistic — installations at roughly nine times the U.S. rate — is the physical expression of this: AI in China is increasingly embodied, not just conversational. The strategic risk for the United States is that it wins the benchmark and loses the install base, the way it once led in mobile hardware but ceded the world's manufacturing floor.

Scorecard, AI: U.S. leads on peak model quality, agentic capability, and the enterprise and capital ecosystem; China leads on cost, openness, patents, publications, physical deployment and talent retention. Advantage: too close to call, and narrowing in China's favor.

Category 2 — Compute: the American moat, and the Chinese workaround

If AI models are the visible product, compute is the factory that makes them, and here the United States still holds its clearest structural advantage — because it controls the best chips and most of the supply chain.

The scale of the American buildout is staggering. In September 2025, OpenAI and Nvidia announced a partnership to deploy at least 10 gigawatts of Nvidia systems, with Nvidia committing up to $100 billion of investment as each gigawatt comes online; the first gigawatt is slated for the second half of 2026 on Nvidia's new Vera Rubin platform. That is one deal. Zoom out and the six largest American AI infrastructure players — Amazon, Google, Meta, Microsoft, Oracle and the Stargate consortium — have committed north of $690 billion in capital expenditure, with 74 new data centers breaking ground across 28 states in 2026 alone. Nvidia hardware now powers more than 400 of the 500 fastest supercomputers in the world, and nine of the ten most energy-efficient systems on the planet.

That last point is the quiet key to the LineShine story. Yes, China's CPU-only machine topped the headline Linpack ranking. But on HPL-MxP, the mixed-precision benchmark that actually reflects AI training workloads, LineShine placed only fourth, at 7.92 exaflops — behind GPU-accelerated systems. LineShine is a monument to Chinese engineering under sanctions, and a genuine achievement. It is not, however, an AI supercomputer in the sense that matters for training frontier models. For the workloads that make ChatGPT and Claude and Gemini, accelerators still rule, and America still makes the best ones.

Which is precisely why China is racing to build its own. DeepSeek's V4, released in April 2026, was the inflection point: the company worked hand-in-glove with Huawei to make the model train and run on Ascend AI processors instead of Nvidia's. The moment DeepSeek proved a frontier-class model could live on domestic silicon, ByteDance, Tencent and Alibaba began scrambling to order Huawei's Ascend 950, and SMIC — the foundry that fabricates those chips — jumped 10% in Hong Kong. The transition is not painless: DeepSeek's anticipated R2 model has reportedly been delayed in part because of the difficulty of training on Ascend hardware. But the direction is unmistakable. China is building a parallel, sanction-proof compute stack, one hard-won generation at a time.

Export controls are the battleground. The Biden-era blanket ban gave way in January 2026 to a case-by-case licensing regime under which Nvidia's H200 — roughly six times as powerful as the previously permitted H20 — could in principle be sold to China. In practice, the picture is a standoff: Washington attached a 25% tariff and extended its restrictions to Chinese firms' overseas subsidiaries, while Beijing has discouraged its own champions from buying American chips at all, preferring to force-feed the domestic ecosystem. Congress, meanwhile, has advanced the "AI OVERWATCH Act" to ban exports of Nvidia's top-end Blackwell chips outright. The net effect is that the world's two largest economies are actively decoupling their compute supply chains — America betting that its chip lead is decisive, China betting it can close the gap before the lead compounds.

The chip itself is only the visible tip of a supply chain America and its allies still dominate. Behind every Nvidia accelerator sits Taiwan's TSMC, which fabricates the most advanced logic on earth; behind TSMC sits the Netherlands' ASML, the sole maker of the extreme-ultraviolet lithography machines required to print those transistors — machines China is barred from buying. And around the processor sit the high-bandwidth memory stacks from SK Hynix, Samsung and Micron that feed data to the compute cores fast enough to keep them busy. Sanction the chip and you have slowed China by a year; sanction the whole tool-chain — lithography, memory, design software — and you have tried to freeze it in place. SMIC, China's leading foundry, can produce advanced-node chips, but without EUV it does so at lower yields and higher cost, which is exactly why DeepSeek's R2 stumbled on Ascend hardware. The American bet is that this tool-chain lead is the most defensible asset in the entire contest.

China's counter-leverage is upstream of everything: raw materials. Beijing has responded to chip restrictions with export controls of its own on critical minerals and rare-earth materials — inputs the West needs for magnets, sensors, and the very manufacturing equipment that makes semiconductors. It is mutual assured disruption: the U.S. controls the high end of the chip stack, China controls the low end of the materials stack, and each can raise the other's costs. That symmetry is why a full decoupling hurts both sides and why, for all the tough talk, licensing regimes keep reopening narrow channels.

There is a wildcard: photonics. Chinese teams have demonstrated optical computing chips — one, dubbed CHIPX, is claimed to run certain AI workloads up to 1,000 times faster than a GPU, with a firm reportedly producing 12,000 wafers a year, though yields remain low. Optical and quantum-photonic approaches are a way for China to leapfrog rather than catch up, sidestepping the transistor-scaling race where U.S. and Taiwanese fabs hold the lead. It is early and unproven at scale, but it is exactly the kind of asymmetric bet a country under sanctions is incentivized to make.

Scorecard, compute: U.S. leads decisively on AI-grade accelerators, energy efficiency, supply-chain control and sheer capital deployed. China leads on self-sufficiency momentum, CPU-class HPC, and a credible photonics wildcard. Advantage: United States — but it is a lead measured in years, not decades, and export controls are accelerating China's escape.

Category 3 — Quantum computing: America's institutions, China's state machine

Quantum is where the rivalry is least mature and most consequential, because a genuine fault-tolerant quantum computer would reset the board — in materials science, in drug discovery, and, ominously, in cryptography. Here the two countries are close to level, and they are getting there by very different routes.

The United States leads on the strength of its private and institutional depth: IBM, Google, IonQ, Quantinuum, PsiQuantum and a dense layer of venture-funded startups, backed by national labs and universities. Washington's June 2026 executive orders were an attempt to convert that private depth into a coordinated national program. The orders reconstituted the National Quantum Initiative Advisory Committee, directed an updated National Quantum Strategy, launched the DOE's QC-ADDS effort to field a science-grade quantum computer by 2028, ordered the Department of War to identify three next-generation quantum-sensor projects within 60 days (with a 2028 fielding target), and gave NASA 120 days to produce a five-year plan for quantum sensing and networking in space. The administration noted it had invested $625 million so far in national quantum research institutes. Separately, NIST and SRI International stood up a Quantum Manufacturing Engineering Center with an initial $20 million to bridge lab research and commercial production.

China's approach is the mirror image: less reliant on a private venture ecosystem, more driven by state direction and national champions. And on the science, it is delivering. In December 2025, a team led by Pan Jianwei at the University of Science and Technology of China crossed the fault-tolerant threshold with the Zuchongzhi 3.2 superconducting processor — the first team outside the United States to reach the point where adding error correction makes the system more stable rather than less. That is a milestone that separates toys from tools. In May 2026, Origin Quantum brought its fourth-generation "Origin Wukong-180" superconducting machine online — a 180-qubit system that it opened to global users and, notably, wired into an AI application ecosystem. China Telecom's photonic Tianyan-P2000 pushed the photon count to 2,682 and put it on a public cloud. And Chinese researchers demonstrated a nine-spin quantum system matching a 10,000-node classical network on a weather-prediction task — the kind of narrow, real-world quantum advantage that hints at practical value long before a universal machine arrives.

Crucially, China has written quantum into its national plan. The 15th Five-Year Plan (2026–2030) explicitly names quantum technology among a handful of "new drivers of economic growth," which in the Chinese system means sustained, patient, state-backed funding regardless of quarterly market sentiment. On the money side, the momentum is visible: China's quantum investment in the first quarter of 2026 nearly matched its entire full-year 2025 total.

There is a defensive dimension to all this that sits squarely in my own field. The second American executive order — "Securing the Nation Against Advanced Cryptographic Attacks" — is about post-quantum cryptography, and it matters because of a threat that does not require a working quantum computer today. "Harvest now, decrypt later" is the practice of adversaries capturing encrypted data now, in the expectation of decrypting it once a cryptographically relevant quantum computer exists. The defense is migration to the NIST-standardized post-quantum algorithms — the FIPS 203, 204 and 205 standards finalized in 2024 — and that migration takes years. Whichever country hardens its critical infrastructure first buys itself strategic insurance; whichever lags leaves its secrets exposed in retrospect. It is the rare arms race where the smart move is to run before the starting gun.

The reason quantum matters commercially, and not just militarily, is worth stating plainly, because the hype has outrun the reality for a decade and skepticism is warranted. A fault-tolerant quantum computer would not replace the GPU for training AI — that is a common misconception. What it would do is solve a narrow class of problems that are effectively impossible for classical machines: simulating molecules and materials from first principles (which would transform battery chemistry, catalysts and drug discovery), certain optimization problems in logistics and finance, and — the one that keeps governments awake — breaking the public-key cryptography that currently secures the internet. The Chinese weather-prediction result, where nine quantum spins matched a 10,000-node classical network at under 1% of the cost of the facility that would normally be required, is a preview of the first category: narrow, real, and economically meaningful well before a universal machine exists. Both countries are chasing these near-term "quantum advantage" demonstrations precisely because they justify the spend long before the fault-tolerant era arrives.

The corporate lineups tell the story of the two systems. On the American side, IBM has published an aggressive roadmap toward error-corrected machines, Google's superconducting program set the early fault-tolerance benchmarks that USTC has now matched, IonQ and Quantinuum lead the trapped-ion approach prized for qubit quality, and PsiQuantum is making a large photonic bet — a diverse, competitive, privately-capitalized field. On the Chinese side, the effort concentrates around USTC's Pan Jianwei group, Origin Quantum, and state-backed entities like China Telecom's quantum arm, funded and coordinated from the center. The American model generates more shots on goal and more architectural diversity; the Chinese model guarantees that whichever architecture wins will be pursued with national resources regardless of the funding cycle. Neither is obviously superior, which is exactly why this race is level.

Scorecard, quantum: U.S. leads on institutional and commercial depth and just moved to coordinate it nationally; China leads on state-directed funding consistency and has matched or beaten the U.S. on several recent hardware and fault-tolerance milestones. Advantage: genuinely even — the closest of the four races.

Category 4 — Power: the race America is quietly losing

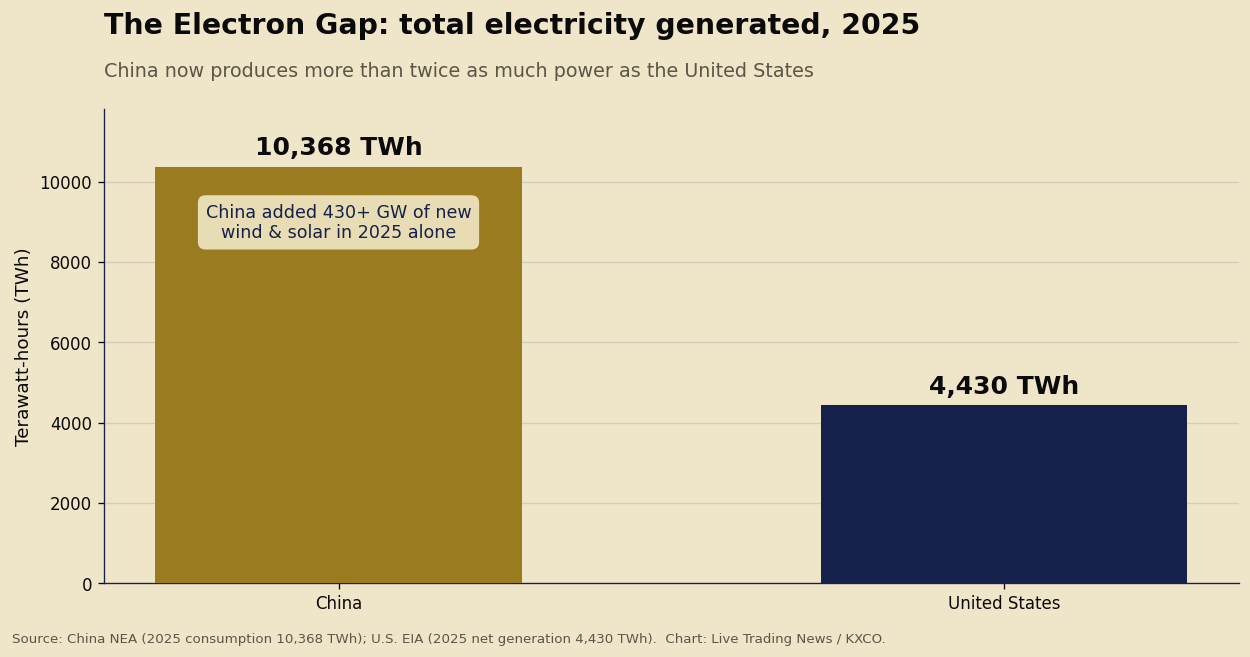

Here is the uncomfortable truth that ties everything together. You cannot run AI without compute, and you cannot run compute without electricity — vast, reliable, around-the-clock electricity. And on power, the United States is not narrowly behind China. It is behind by a factor of more than two, and the gap is widening.

In 2025, China's electricity consumption topped 10,368 terawatt-hours for the first time, up 5% on the year. The United States generated 4,430 terawatt-hours, a record for America but up just 2.8%. China produces more than twice the power of the United States, and it is adding capacity at a pace the U.S. cannot presently match: over 430 gigawatts of new wind and solar in 2025 alone, lifting installed renewable capacity above 1,800 GW, within a total generating fleet north of 3,600 GW. More than half of China's electricity growth over the past decade has come from clean sources — wind, solar and hydro. This is the phenomenon analysts have started calling the "electron gap," and multiple observers returning from China have described the contrast with America's aging, congested grid in stark terms.

The demand side is where it bites. Worldwide data-center power demand is set to rise about 27% in 2026, reaching 132 GW (up from 104 GW in 2025) and heading toward roughly 290 GW by 2030. Both countries are scaling data-center electricity consumption fast — U.S. data-center demand is projected to more than double by 2030, reaching around 426 TWh, or roughly 9% of all U.S. electricity; China's data-center consumption is on a similar doubling trajectory, toward 277–289 TWh by 2030, growing about 19% a year. The difference is not the rate of growth in demand. The difference is the ease of supplying it.

China treats power as solved infrastructure. Its 2026–2030 plan makes data-center buildout a strategic priority and requires new projects in its eight national computing hubs to source at least 80% of their power from renewables. China can simply add generation faster than its data centers consume it. The United States cannot — the binding constraint on American AI is now the grid, not the chips. Interconnection queues stretch for years, transmission is congested, and in some regions the grid is too weak to absorb a hyperscale campus at all.

The American response is revealing, and it is a scramble. Because grid upgrades and new nuclear take years, the fastest path to power has become behind-the-meter natural gas — on-site gas turbines that can be deployed in 12 to 18 months, bypassing the grid entirely. Natural gas already supplies an estimated 40–45% of U.S. data-center electricity. In parallel, the industry is reaching for nuclear: Microsoft signed a 20-year deal tied to the restart of Three Mile Island Unit 1, and Amazon secured access to nearly 2 GW of nuclear via Talen Energy. Small modular reactors are the great hope, but they carry 5-to-10-year lead times and heavy regulatory and capital burdens. The tell is that some American companies have concluded the grid is such a bottleneck that they are building their own power plants rather than waiting for utilities to catch up.

Scorecard, power: China leads decisively — more than double the generation, faster additions, cleaner mix, and power treated as a solved problem rather than a constraint. The U.S. is improvising with gas and betting on a nuclear revival that is real but slow. Advantage: China, and this is the category where its lead is largest and most durable.

The rate of growth: who is accelerating faster

A scorecard is a snapshot; the more important question is the derivative — who is speeding up. On this, the two countries diverge in an instructive way.

The United States is growing fastest where capital can move fastest: private investment and data-center construction. That $690 billion-plus of committed hyperscaler capex, the $100 billion Nvidia-OpenAI arrangement, 74 data centers breaking ground in a single year — this is the fastest deployment of private capital into a single technology in history. When the input is money and the output is buildings and chips, America is unmatched, because it has the deepest capital markets on earth and a venture ecosystem tuned to exactly this.

China is growing fastest where the state can direct resources and where physical industrial capacity compounds: electricity generation (roughly 6% a year for a decade, off a base already twice America's), renewable installation (430+ GW in one year), chip self-sufficiency (from near-total Nvidia dependence to frontier models on domestic Ascend silicon in about two years), patents, publications, and robot deployment. China's model-quality gap to the U.S. shrank from ~30 points to under 3 in under three years — arguably the fastest catch-up in the history of the field. And its quantum funding roughly doubled its run-rate in a single quarter.

The synthesis: America's growth is capital-led and concentrated at the frontier; China's is industrially-led and broad-based. In a race decided by who has the single most capable model next year, the U.S. edge in capital and talent probably prevails. In a race decided by who can deploy AI across an entire economy — cheaply, at scale, powered reliably — China's advantages in cost, openness, manufacturing and electricity compound in its favor. The former is a sprint; the latter is a marathon, and the marathon is the one that reshapes GDP.

The hidden front: who the rest of the world adopts

There is a fifth contest hiding inside the four, and it may matter most of all: the battle for global adoption. The United States and China are not just building AI for themselves — they are competing to become the default AI supplier for everyone else, and the mechanics of that competition favor different players than the benchmark race does.

China's open-weight, low-cost strategy is, among other things, a distribution weapon aimed squarely at the Global South and the price-sensitive middle of the world economy. A developer in Jakarta, Lagos, São Paulo or Karachi who can download a near-frontier model for free and run it for a sixth the price of the American alternative will do so — and once a country's startups, universities and ministries build on a given stack, they tend to stay on it. That is how standards and dependencies form. The United States counters with the trust, reliability, security guarantees and cloud integration that large enterprises and Western governments require, plus the raw capability advantage for the hardest tasks. The likely outcome is not one winner but a partitioned world: an American-aligned AI sphere and a Chinese-aligned one, split along the same lines as the chip supply chains. For every country and company outside the two superpowers, the strategic imperative becomes optionality — the ability to run on both stacks and avoid being captured by either.

Talent is the other quiet front. The reversal of the brain drain — AI researcher migration to the U.S. down nearly 90% since 2017 — is a slow-acting but profound shift. The American research advantage was built substantially on importing the world's best minds, including a large share of China's. If that pipeline is narrowing while China's domestic universities and labs mature, the compounding effect over a decade is significant. Research leadership is a lagging indicator; by the time it shows up in the model rankings, the underlying talent shift is already years old.

What the scorecard actually says

Put the four categories together and the caricature of "America is winning the AI race" dissolves into something more precise and more interesting:

AI models: U.S. ahead on quality by a whisker (2.7%); China ahead on cost, openness, patents, publications and deployment. Trending China's way.

Compute: U.S. ahead clearly on AI-grade chips, efficiency and capital; China building a credible sanction-proof alternative and holding a photonics wildcard. U.S. lead, eroding.

Quantum: Dead even. U.S. institutional depth versus Chinese state consistency and recent hardware milestones.

Power: China ahead decisively and durably — more than double the generation and adding capacity faster.

The uncomfortable conclusion for American strategists is that the two categories where the U.S. lead is clearest — model quality and chips — are also the two most vulnerable to erosion (models via China's efficiency-and-openness strategy, chips via export controls that are accelerating Chinese self-sufficiency). Meanwhile the category where China leads most decisively — power — is the one that is hardest and slowest to change, because you cannot venture-fund your way to a national grid in eighteen months. Money builds data centers quickly; it does not build transmission lines, permitting reform, or 3,600 gigawatts of generating capacity quickly.

That is the real message of the last week of June 2026. LineShine topping the supercomputer list without American chips, DeepSeek running on Huawei silicon, China Telecom's photonic quantum cloud, and China's yawning electricity lead all point the same direction: the U.S. is still ahead at the frontier, but China has built the industrial and energy base to contest — and in some categories win — the long game. Washington's quantum executive orders and the trillion-dollar private buildout are serious answers. Whether they are fast enough answers depends less on who trains the smartest model in 2027 and more on who can plug it in.

For businesses and investors, the strategic takeaways are concrete. First, assume a bifurcated world: two AI stacks, two chip supply chains, two sets of standards, and plan for interoperability across both rather than betting everything on one. Second, watch power as the leading indicator of AI capacity — the electron gap is the most under-priced variable in the entire race, and grid access is becoming the real moat. Third, treat post-quantum security as a present-tense obligation, not a future one; the harvest-now-decrypt-later clock is already running, the NIST standards exist, and the migration is measured in years. The countries — and companies — that internalize those three realities now will be the ones still standing when the scorecard is tallied at the end of the decade.

The race is not over, and it is not one race. It is four. Right now the United States and China are each winning two.

Sources

Euronews — "World's fastest supercomputer is now from China, surpassing US and Germany" (24 June 2026): https://www.euronews.com/next/2026/06/24/worlds-fastest-supercomputer-is-now-from-china-surpassing-us-and-germany

Tom's Hardware — "China bypasses US GPU bans with 1.54-exaflops 'LineShine' supercomputer" / CPU-only exascale coverage: https://www.tomshardware.com/tech-industry/artificial-intelligence/china-bypasses-us-gpu-bans-with-1-54-exaflops-lineshine-supercomputer-cpu-only-monster-packs-2-4-million-huawei-designed-armv9-cores

The Next Platform — "A Deep Dive On China's 'LineShine' All-CPU, Exaflops-Class Supercomputer" (25 June 2026): https://www.nextplatform.com/hpc/2026/06/25/a-deep-dive-on-chinas-lineshine-all-cpu-exaflops-class-supercomputer/

The White House — "Ushering in the Next Frontier of Quantum Innovation" (Executive Order, 22 June 2026): https://www.whitehouse.gov/presidential-actions/2026/06/ushering-in-the-next-frontier-of-quantum-innovation/

The White House — Fact Sheet on the quantum innovation order: https://www.whitehouse.gov/fact-sheets/2026/06/fact-sheet-president-donald-j-trump-ushers-in-the-next-frontier-of-quantum-innovation/

The White House — "Securing the Nation Against Advanced Cryptographic Attacks" (Executive Order, 22 June 2026): https://www.whitehouse.gov/presidential-actions/2026/06/securing-the-nation-against-advanced-cryptographic-attacks/

PostQuantum.com — "Trump Orders National Quantum Computer Build at DOE" (QC-ADDS, 2028 target): https://postquantum.com/quantum-policy/trump-quantum-innovation-executive-order/

The Quantum Insider — "China's New Five-Year Plan Specifically Targets Quantum Leadership And AI Expansion": https://thequantuminsider.com/2026/03/05/chinas-new-five-year-plan-specifically-targets-quantum-leadership-and-ai-expansion/

Global Times — "Chinese company launches 4th-generation superconducting quantum computer" (Origin Wukong-180): https://www.globaltimes.cn/page/202605/1360606.shtml

South China Morning Post — "Chinese team shows quantum tech can disrupt AI in a real-world task": https://www.scmp.com/news/china/science/article/3349995/chinese-team-shows-quantum-tech-can-disrupt-ai-real-world-task

Stanford HAI — 2026 AI Index Report: https://hai.stanford.edu/ai-index/2026-ai-index-report

The Next Web — "Stanford AI Index 2026: China narrows US lead to 2.7% while spending 23x less on AI investment": https://thenextweb.com/news/stanford-ai-index-2026-china-us-performance-gap

Fortune — "DeepSeek unveils V4 model, with rock-bottom prices and close integration with Huawei's chips": https://fortune.com/2026/04/24/deepseek-v4-ai-model-price-performance-china-open-source/

CSIS — "DeepSeek, Huawei, Export Controls, and the Future of the U.S.-China AI Race": https://www.csis.org/analysis/deepseek-huawei-export-controls-and-future-us-china-ai-race

NVIDIA Newsroom — "OpenAI and NVIDIA Announce Strategic Partnership to Deploy 10 Gigawatts of NVIDIA Systems": https://nvidianews.nvidia.com/news/openai-and-nvidia-announce-strategic-partnership-to-deploy-10gw-of-nvidia-systems

ValueAdd VC — "AI CapEx Tracker 2026: $690B, 74 Data Centers Mapped": https://valueaddvc.com/ai-buildout-tracker

Gartner — "Data Center Electricity Consumption to Grow 26% in 2026" (press release, 10 June 2026): https://www.gartner.com/en/newsroom/press-releases/2026-06-10-gartner-says-data-center-electricity-demand-to-grow-26-percent-in-2026

Rystad Energy — "China's data center capacity set to top 60 GW by 2030, driving a doubling of power demand": https://www.rystadenergy.com/news/chinas-data-center-capacity-doubling-of-power

Carbon Brief — "Explainer: How China is managing the rising energy demand from data centres": https://www.carbonbrief.org/explainer-how-china-is-managing-the-rising-energy-demand-from-data-centres/

Brookings — "How will the United States and China power the AI race?": https://www.brookings.edu/articles/how-will-the-united-states-and-china-power-the-ai-race/

S&P Global — "China's 2025 power consumption tops 10 trillion kWh for first time: NEA": https://www.spglobal.com/energy/en/news-research/latest-news/energy-transition/011926-chinas-2025-power-consumption-tops-10-trillion-kwh-for-first-time-nea

Enerdata / U.S. EIA — "US electricity generation hits new record at 4,430 TWh in 2025": https://www.enerdata.net/publications/daily-energy-news/us-electricity-generation-hits-new-record-4430-twh-2025-says-eia.html

U.S. EIA — "U.S. electricity generation in 2025 hit a record, again": https://www.eia.gov/todayinenergy/detail.php?id=67284

Utility Dive — "AI is outpacing America's power grid. Nuclear must become a national priority.": https://www.utilitydive.com/news/ai-power-grid-nuclear-national-priority/811744/

Computer Weekly — "AI chip restrictions limit Nvidia H20 China exports": https://www.computerweekly.com/news/366622857/AI-chip-restrictions-limit-Nvidia-H20-China-exports

LM Council — AI Model Benchmarks, July 2026 (GPT-5.5, Claude Opus 4.8, Gemini 3.1, Grok 4.3): https://lmcouncil.ai/benchmarks

Tom's Hardware — "New Chinese optical quantum chip allegedly 1,000x faster than Nvidia GPUs" (CHIPX): https://www.tomshardware.com/tech-industry/quantum-computing/new-chinese-optical-quantum-chip-allegedly-1-000x-faster-than-nvidia-gpus-for-processing-ai-workloads-but-yields-are-low

Figures verified as of 4 July 2026. Where sources report ranges or preliminary data (e.g. data-center demand projections and model-benchmark scores), the article states the most widely reported figure and attributes it. AI model rankings change frequently; benchmark standings reflect mid-2026 reporting.

Understanding the US China AI and Quantum Landscape

AI and quantum are usually reported as a US–China race. The more useful story is two different systems — frontier capital versus open-source scale — entangled through shared chokepoints. Shayne Heffernan maps the landscape with the KXCO AI Sector Ontology, with comparison graphics and the investable names.

KXCO Upgrades Its Post-Quantum Security Stack to the Full NIST Trio

KXCO has completed the full NIST post-quantum trio — adding hash-based SLH-DSA (FIPS 205) to ML-KEM and ML-DSA and modernising the engine — hardening quantum security across every product, with the whole foundation open and independently verifiable on npm and GitHub. By Shayne Heffernan.

SpaceX: The AI Company You Might Be Missing

The market watches Falcon 9 and Starlink; it is missing the AI company SpaceX has quietly built — xAI, Colossus, the $55bn Terafab chip fab and orbital data centres. Shayne Heffernan maps SpaceX's position against the KXCO AI Sector Ontology ahead of its IPO.

TSMC $TSM at the Heart of the AI Boom

TSMC plans to raise chipmaking prices 5–10% from 2027 and its customers are not walking away. The KXCO ontology shows why: TSMC is the chokepoint the entire AI economy passes through. The sector is just beginning, and TSM is the ideal way to own it.

Every story, signed and delivered.

Subscribe to the kxco channel and get the headline, the AI-written key takeaways, and the chain-anchor link the moment we publish. Audio versions and per-ticker subscriptions arrive in the next iteration.